Traditional company pension plans (bAV) often add little value. We are changing that - with the ginkgo bAV. ETF-based. Commission-free. Fully digital.

In line with EU standards

Based in the heart of Berlin

Permission in accordance with §34d GewO

In line with EU standards

Based in the heart of Berlin

Permission in accordance with §34d GewO

Company pensions (bAV) often are not yet a valuable part of compensation for SMEs. Why is that?

Expensive bAV contracts

Lack of transparency and high costs

Push 1:1 sales

Hidden sales commissions

Weak user experience

One letter per year - pension “out of mind”

High admin effort

Complex implementation

For company pensions to become a truly valued part of compensation, modern high-performing financial products are needed - that are fully visible to employees.

Modern financial product

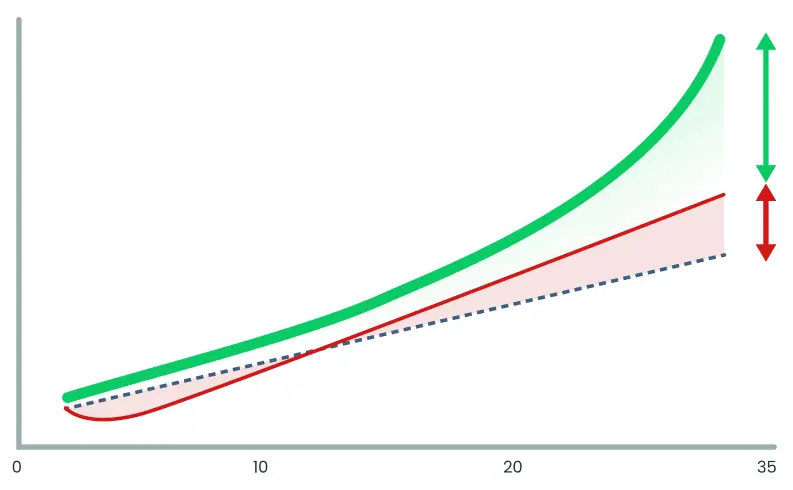

Commission-free and ETF-based - for better returns & higher pensions

Innovative app for employees

For real-time transparency on company pensions at all times

Digital platform for people/HR

For maximum efficiency — unlocking the full bAV potential

Efficient rollout in the company

For maximum impact with minimum effort

The ginkgo bAV is a modern financial product: ETF-based, commission-free and with low running costs. Because bAV also deserves modern financial products.

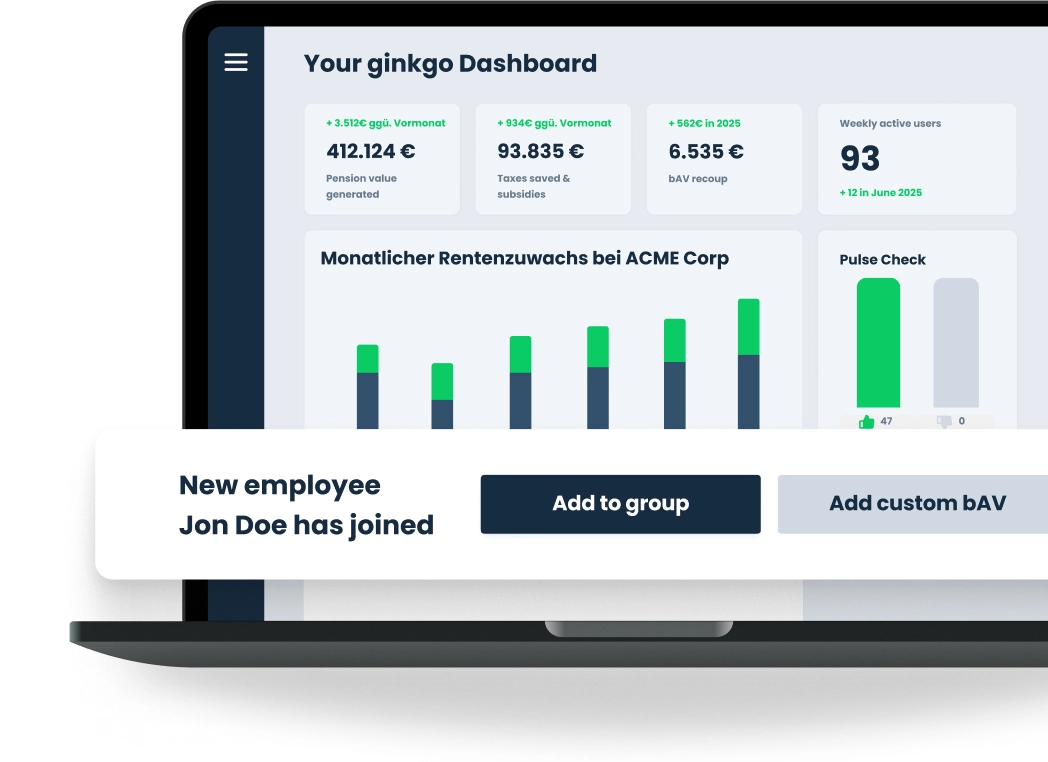

With the ginkgo app, employees have 24/7 access to their company pension, with full transparency regarding contributions and fees. This keeps bAV always top-of-mind and allows for easy and flexible management, such as adjusting contributions at any time.

On the ginkgo platform for people/HR, all events relating to bAV are automatically recorded and processed digitally. Integration with HRIS & Payroll takes <30 minutes. This keeps bAV admin for people/HR to a minimum.

Using an API or ASCII interface, ginkgo can be integrated with over 40 HRIS and payroll systems — for maximum quick set-up.

ginkgo supports or takes over the entire launch process. With suitable materials and launch sessions, tailored to your company — for effective and authentic communication.

Our team of experts is always available to answer technical or subject-related questions about bAV — before and after the launch. This way, ginkgo takes the complexity of bAV completely off your plate.

Together with the company, ginkgo defines the optimal bAV program — with professional expertise, market benchmarks and, if necessary, budgeting support.

ginkgo takes over the complete technical set-up, including seamless integration with existing HR and payroll systems.

ginkgo takes care of planning and provides communication materials and formats to optimally prepare employees & HR teams for launch.

The new bAV goes live. ginkgo delivers the launch presentation, hosts Q&A sessions, and drives employee activation. For a successful start.